Early Bird

Deadline

June 30, 2026

Judging

Date

November 11, 2026

Winners

Announcement

November 26, 2026

Thailand ranks as an emerging wine market, yet this label captures only part of its potential. It boasts enough infrastructure to sustain sophisticated importers, fine wine lists, and premium retail, while regulations, pricing, and hospitality-led consumption continue to shape its trajectory. Unlike nascent markets lacking wine culture or mature ones like South Korea and Japan, Thailand occupies a strategic middle ground.

The market is fully import-driven, where success hinges on distribution, pricing, premium hospitality visibility, and local execution. In 2024, Thailand imported about $133 million of wine, led by France, Australia, Italy, the United States, and Chile. Urbanization and a rising middle class with greater disposable incomes are fueling expansion, while digital platforms now enable direct shipments from small European producers to Asian consumers, bypassing traditional barriers and cutting costs (Source).

The Thai market for imported bottled wine grew by 6.24% in value between 2024 and 2025, reaching 3.72 billion THB (100.27 million EUR); overall imported wine hit 6.54% growth in 2025 to a CIF value of 4.72 billion THB (127.22 million EUR). Bangkok, Phuket, hospitality, tourism, high-end dining dominate, with recent tariff and excise changes improving economics—positioning it as a premium arena for channel-savvy producers (Source).

Convention dictates that beer and whiskey dominate palates and in 2024, beer captured over 80% of on-trade volumes in premium-and-above bands, with blended Scotch driving a third of spirits value in bars, per IWSR on-trade data. Yet shifts are underway: wine and white spirits (fueled by cocktail culture) are gaining ground, as beer imports decline against local brands and blended whisky loses appeal. “Thailand’s beer category remains resilient, popular with locals and tourists, as home-grown brands elevate their positioning,” notes Jalene Teng, IWSR Senior Market Analyst. “Wine is maturing as consumers gravitate toward it, while white spirits like tequila, rum, vodka, and gin thrive in cocktail bars.”

Thailand's importance stems not from volume but from tourism, urban dining, and premium hotels. Bangkok leads as the wine hub, with Phuket and other tourist spots amplifying demand via hotels, restaurants, and international traffic. The USDA pegs Thailand's 2024 foodservice market at $35.4 billion, buoyed by tourism recovery—a key driver for wine amid tax complexities.

In 2024, Thailand imported $139M of Wine, becoming the 36th largest importer of Wine (out of 225) in the world. During the same year, Wine was the 299th most imported product (out of 1,217) in Thailand. In 2024, Thailand imported Wine primarily from: France ($55M), Australia ($31.5M), Italy ($20M), United States ($9.68M), and Chile ($8.34M). The fastest growing origins for Wine imports in Thailand between 2023 and 2024 were: France ($8.24M), Italy ($2.42M), and Japan ($163k). (Source)

This access underscores that supply is not the barrier, but distribution to the right importers, hospitality groups, and occasions is.

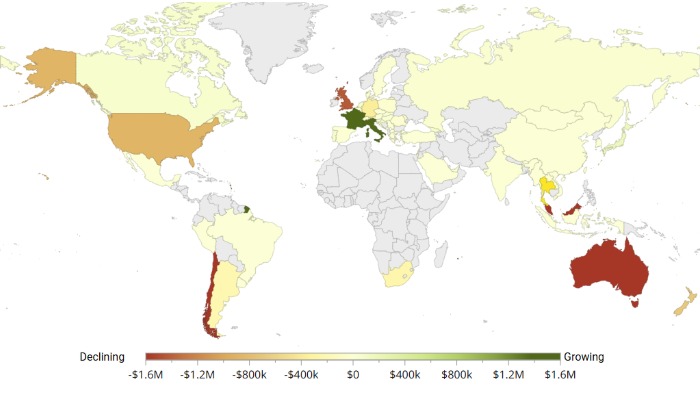

The map shows the market growth of wine imports to Thailand between 2023-24 (Source: OEC)

Thailand's 2024 reforms eliminated tariffs on HS 2204 and 2205 wines—previously 54% for <23% ABV and 60% for a higher ABV from non-FTA countries—and restructured excises, slashing U.S. wine retail prices by 35-40%, per USDA. These cuts broaden product access and origins, boosting still wine volumes +3% in 2024 (IWSR) with a +3% CAGR to 2029; sparkling grew +3% but moderates to +1% CAGR.

Chile and Australia lead via FTAs, but U.S. and Italian wines benefit most—Italy up +9% in 2024, ahead of New Zealand (+7%), Australia (+3%), and Chile (+1%), thanks to fresh profiles. “Thai consumers favor wine over brown spirits for health benefits and lower intoxication, viewing it as ‘age-defying,’ especially among women and urban professionals,” says Teng. “It's now tied to social dining, wine bars, events, bottle shops, and festivals” (Source).

Prices remain sensitive post-reform, but importers gain flexibility for hospitality and retail viability, warranting a reassessment for brands dormant in Thailand.

Distribution gates success in this importer-led, relationship-driven market. To offer an overview of the importing map, Italasia imports five million bottles yearly with nationwide dealerships (Source); Ambrose Wine & Spirits, The Wine Merchant, Wine Garage, and IWS Thailand have built and continue to maintain a strong relationship with hotels, restaurants, and retail across the country. In the event that passive supply fails, importers actively forge placements, ensuring that product is moving through the supply chain rather than stuck in inventory. It is for this very reason, picking the right partner to enter the market becomes a necessary step.

Thailand has meaningful wine retail, but the market is still strongly influenced by hospitality and tourism. That is one reason wine behaves differently here than in South Korea, where mass retail and convenience stores are far more central to category growth. In Thailand, premium dining, hotels, rooftop venues, and tourism-facing foodservice still play an outsized role in introducing wines to consumers and reinforcing brand value. USDA’s Thailand foodservice reporting makes clear that Thailand's hospitality market will grow from $22.68 billion in 2025 to $36.26 billion by 2031 (8.13% CAGR) (Source).

That does not mean retail is irrelevant. Far from it. Chains and specialty operators help drive availability and repeat purchase, especially in Bangkok. Wine Connection describes itself as the leading chain of wine shops and wine-themed restaurants in Southeast Asia, with a visible presence in Thailand. Wine Gallery Thailand says it has four shops in Bangkok and one in Chiang Mai, plus warehousing and operations in multiple cities. King Power Duty Free is also relevant for premium wine and spirits exposure through airports and travel retail. These channels matter not only for sales, but for brand visibility among both residents and travelers.

Thailand is not a broad-based, daily wine consumption market. Wine remains concentrated among urban professionals, affluent Thai consumers, expatriates, tourists, and hospitality occasions. That means brands are often selling into a consumer base that is interested, aspirational, and willing to spend—but not necessarily loyal in the way consumers in traditional wine markets may be.

This creates a market where occasion and context matter enormously. Wine is tied to dinners out, hotel consumption, business entertaining, gifting, and premium leisure occasions. That favors producers who understand that Thailand is not just a country market, but a hospitality market. Wines that work on lists, pair with international cuisine, and fit premium but understandable price points are more likely to perform than wines that rely purely on heritage messaging. The supplier mix shown in Thailand’s import data reinforces this: prestige-producing countries lead, but the market is not exclusively luxury. It is a layered premium market with room for value and mid-tier wines if they are correctly positioned.

Wine is tied to dinners out, hotel consumption, business entertaining, gifting, and premium leisure occasions

One of the reasons Thailand is strategically important is that tourism amplifies wine demand in ways that domestic consumption figures alone may not capture. Hotels, resort dining, airport retail, and premium foodservice create occasions where imported wine becomes part of an international hospitality offer. This is why destinations like Phuket matter alongside Bangkok. Producers are not just selling into local retail shelves; they are selling into a broader leisure and travel economy. USDA explicitly ties foodservice growth to the recovery of the tourism sector, which is highly relevant for imported wine.

This also affects portfolio strategy. Producers need to think about where their wines fit: upscale resort dining, mid-premium restaurant lists, retail gifting, or specialist merchant channels. Thailand rewards brands that know their lane. A wine built for by-the-glass in a busy hospitality setting is solving a different problem from a fine wine label targeting allocations through specialist merchants.

Thailand may be more premium-facing than some Southeast Asian markets, but pricing discipline still matters. The 2024 tax reform improved the economics of imported wine, yet final consumer pricing remains highly sensitive. In a market where imported wines compete with spirits, cocktails, beer, and other leisure spending, producers need to be realistic about what their wine looks like at the final list or shelf price.

This is one reason France can dominate premium imports while Australia, Italy, Chile, and the United States remain relevant in different segments. Thailand is not one monolithic premium market. It has prestige buyers, but it also has commercially driven importers and operators who need wines that move, not just wines that impress on paper. A wine that is too expensive for its perceived value will struggle, even if the liquid quality is high.

Brands that succeed in Thailand usually do a few things well. They work with importers that understand hospitality, not just warehousing. They support the market with visibility, education, and relationship-building. They understand whether they belong in hotels, specialist retail, broader restaurant programs, or duty free. And they recognize that Thailand is a market where premium cues matter, but commercial practicality matters just as much.

Thailand also rewards consistency. Because the market is importer-led and hospitality-shaped, wines that stay visible across accounts, lists, and retail touchpoints have a better chance of building recognition. The market is not so large that brands can rely on brute-force volume. It is one where reputation is accumulated through the right placements and sustained execution.

Wine Gallery Thailand (importer) has four shops in Bangkok and one in Chiang Mai, plus warehousing and operations in multiple cities

Thailand is not the biggest wine market in Asia, and it is not the simplest. But it is one of the more strategically interesting ones. It combines a fully import-driven structure, a meaningful premium consumer base, a strong hospitality sector, and improving economics for imported wine after the 2024 tax changes.

Wine succeeds via elite distribution, pricing, and partners. Vice President of IQ Wine and Wine Gallery Thailand, Jerome Chambon, highlights key trends with implications for producers:

• Preference for Finished Products: Bulk imports stagnated at +1% growth, while bottled wine surged 6.24% in value. This signals importers and consumers demanding ready-to-sell, origin-bottled wines over local filling, reducing logistics risks and appealing to premium hospitality seeking authenticity.

• Diversification and Premiumization: Australia (prior volume leader) fell -16.9% in value; Italy exploded +35%, and German wines hiked prices 51%. Producers should prioritize diverse, quality-driven origins over entry-level volume, targeting urban buyers upgrading to fruity, higher-end profiles.

• Market Rationalization: France boosted volumes ~19.7% but cut average bottle prices 10%. Even prestige origins must balance accessibility with premium perception to capture share in a maturing, price-aware landscape favoring value-for-money growth.

• Growth Outlook: Wine expands at beer and spirits' expense, with strong potential ahead. Importers can leverage this by stocking versatile portfolios for hospitality and retail, capitalizing on health trends and social occasions.

Asia's markets demand trade-savvy positioning. Asia Wine Ratings delivers insights, buyers, and intelligence for brands targeting real sales success.

Header image created with AI.

Enter your wines before June 30, 2026, to get the early bird pricing. Enter Your Wines.